Introduction: Why an Emergency Fund is Essential

Life is unpredictable. From sudden medical expenses to unexpected car repairs or even job loss, financial emergencies can happen when you least expect them.

This is why having an emergency fund is crucial. It acts as a financial cushion that provides peace of mind and prevents you from falling into debt when unexpected expenses arise.

In this comprehensive guide, we will walk you through the steps to build an emergency fund that aligns with your financial goals and lifestyle.

Whether you are starting from scratch or looking to enhance your existing savings, this article will provide you with actionable strategies to create a reliable financial safety net.

Understanding an Emergency Fund

Before you start saving, it’s important to understand what an emergency fund is and what it should be used for.

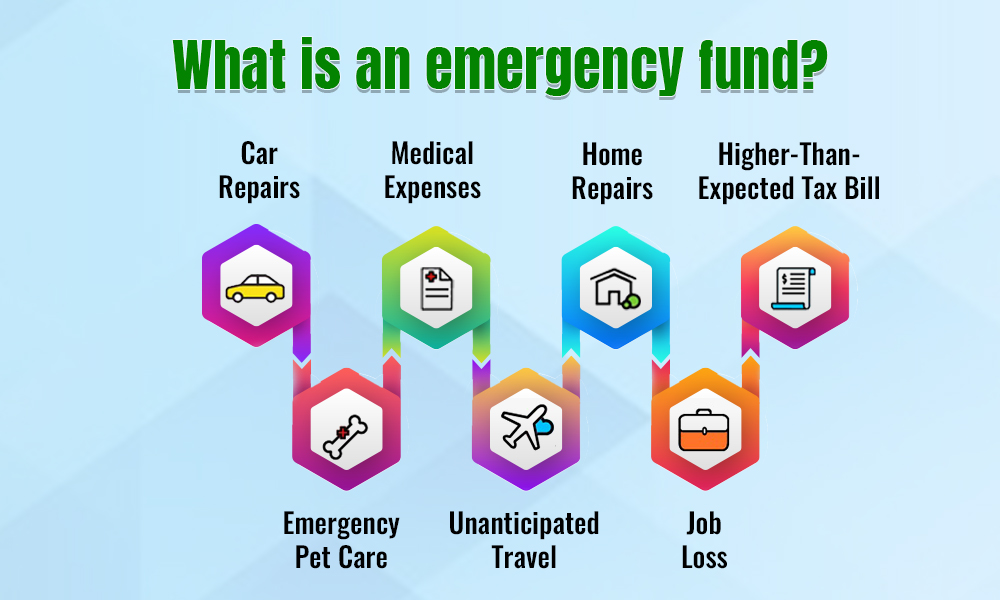

What is an Emergency Fund?

An emergency fund is a pool of money set aside to cover unexpected financial expenses.

Unlike savings for planned expenses like vacations or a new car, this fund is strictly for unplanned emergencies such as:

- Medical emergencies

- Home or car repairs

- Sudden job loss

- Urgent travel expenses

- Unexpected bills

How Much Should You Save?

The amount you should save depends on your financial situation, monthly expenses, and risk factors.

A general rule of thumb is to have at least three to six months’ worth of living expenses in your emergency fund.

However, if you have a fluctuating income or high financial obligations, you may need to save more.

Steps to Build Your Emergency Fund

Now that you understand the importance of an emergency fund, let’s dive into the steps to build one effectively.

1. Assess Your Current Financial Situation

Before setting a savings goal, analyze your income, expenses, and debts. Track your monthly expenses to determine how much you need for essentials like rent, groceries, utilities, and insurance.

This will help you decide how much you should aim to save.

2. Set a Realistic Savings Goal

Break your ultimate savings goal into smaller, manageable milestones. For example, if you want to save $6,000 in a year, aim to save $500 per month or roughly $125 per week.

Setting achievable goals will keep you motivated and help you stay on track.

3. Create a Budget That Prioritizes Savings

A budget is essential for effective financial management. Allocate a portion of your income toward your emergency fund before spending on non-essentials.

You can use the 50/30/20 budgeting rule:

- 50% for necessities (rent, groceries, bills)

- 30% for wants (entertainment, dining out)

- 20% for savings and debt repayment

If necessary, adjust your spending to allocate more toward savings.

4. Automate Your Savings

Setting up automatic transfers to your emergency fund ensures consistency.

You can arrange for a percentage of your paycheck to be deposited into a separate savings account every month.

This “out of sight, out of mind” approach prevents you from spending the money impulsively.

5. Cut Unnecessary Expenses

Look for areas where you can reduce spending. Some ways to free up extra money include:

- Cooking at home instead of eating out

- Canceling unused subscriptions

- Buying generic brands instead of name brands

- Reducing impulse purchases

Redirect the money saved from these small cuts into your emergency fund.

6. Boost Your Income

If your current income does not allow for substantial savings, consider finding additional sources of income. Some options include:

- Taking up a part-time job or freelance work

- Selling unused items online

- Participating in paid surveys or gig work

Using extra income sources can help you build your emergency fund faster.

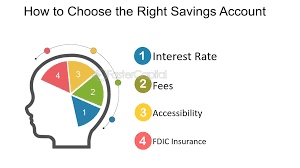

7. Choose the Right Savings Account

Not all savings accounts are created equal. Look for an account that offers:

- Easy access in case of emergencies

- High-interest rates to maximize growth

- No or low fees

Some ideal options include high-yield savings accounts or money market accounts.

8. Stay Committed and Review Regularly

Building an emergency fund requires discipline. Regularly review your savings progress and make adjustments if needed.

Celebrate small milestones to keep yourself motivated. Life circumstances change, so reassess your target savings amount annually.

Overcoming Common Challenges

Building an emergency fund can be challenging, but overcoming obstacles will make you more financially resilient.

What If You’re Living Paycheck to Paycheck?

If you have limited funds, start small. Even saving $5 or $10 per week adds up over time. Focus on increasing your income and cutting unnecessary expenses gradually.

What If You Need to Use Your Emergency Fund?

If you withdraw from your emergency fund, replenish it as soon as possible. Treat it like a mandatory expense and prioritize rebuilding it.

What If Unexpected Expenses Keep Arising?

It’s normal to face financial setbacks. If emergencies occur frequently, review your spending habits and identify areas where you can cut costs or increase your income.

Maintaining and Growing Your Emergency Fund

Once you’ve built your emergency fund, it’s important to maintain and grow it over time.

Keep It Separate from Your Regular Accounts

Avoid using your emergency fund for non-emergency expenses by keeping it in a separate account. This prevents the temptation of dipping into it for everyday expenses.

Continue Saving Even After Reaching Your Goal

Once you’ve reached your savings goal, consider increasing it over time. The more you save, the better prepared you’ll be for any financial crisis.

Invest Any Extra Savings

If you have excess savings beyond your emergency fund, consider investing in retirement accounts or other low-risk investment options to grow your wealth.

A Smart Financial Safety Net: Final Thoughts

An emergency fund is one of the most important tools for financial stability. It provides security, prevents debt, and gives you the confidence to handle unexpected situations.

By following these steps, you can build a financial safety net that works for you. Start today, stay consistent, and watch your emergency fund grow over time.

Frequently Asked Questions (FAQ)

1. How much should I save in my emergency fund?

A good rule of thumb is to save at least three to six months’ worth of living expenses. However, your individual needs may vary based on your income, financial responsibilities, and job stability.

2. Where should I keep my emergency fund?

A high-yield savings account is a good option as it provides easy access while earning interest. Avoid keeping emergency funds in investment accounts, as they may fluctuate in value.

3. How can I save if I have a low income?

Start small, even if it’s just $5 or $10 per week. Cut non-essential expenses and look for ways to increase your income through side jobs or freelance work.

4. Should I pay off debt or build an emergency fund first?

It’s wise to save a small emergency fund (around $500–$1,000) before aggressively paying off debt. Once you have a basic safety net, you can balance debt repayment and savings.

5. What if I need to use my emergency fund?

If you use your emergency fund, make it a priority to replenish it as soon as possible. Adjust your budget to allocate funds toward rebuilding your safety net.

Building an emergency fund takes time and effort, but the financial security it provides is well worth it. Start today and create a savings plan that ensures a stable and stress-free future.